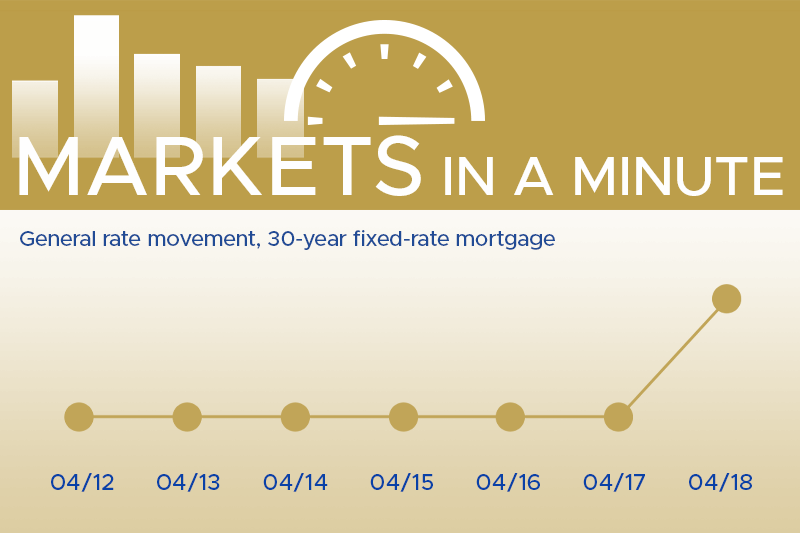

Welcome to our weekly roundup, where we bring you the latest housing market and economic…

More Than Just a Mortgage: A Handy Guide to Home Ownership Expenses

Becoming a homeowner is a significant and exciting milestone, but it’s essential to understand that home ownership expenses extend far beyond the monthly mortgage payment. To ensure financial preparedness, let’s explore the various costs associated with home ownership.

Local Property Taxes:

Local Property Taxes: Towns and cities collect property taxes to fund community services like schools, roads, and parks. The amount you pay depends on your home’s value and local rates. Stay on top of payments to avoid surprise bills. Many mortgages require you to set up an escrow account, where a portion of your monthly payment goes toward your property taxes and homeowner’s insurance. The lender manages the escrow account and makes the tax and insurance payments for you when they are due. This arrangement helps ensure these significant home ownership expenses don’t get overlooked and prevents lump sum payments that can be difficult to budget for. More info

Homeowners Insurance Premiums:

Get coverage in case disaster strikes. Your premium costs vary based on factors like your location, chosen policy, and home details. Comprehensive plans offer the best financial protection.

Maintenance and Repair Expenses:

As a homeowner, you’re responsible for lawn care, HVAC maintenance, gutter cleaning, and more. Also budget for unforeseen repairs like leaky roofs or broken appliances. A common rule of thumb is to budget 1%-4% of a home’s value for annual maintenance. That’s a pretty wide range, but the ideal amount really depends on the age and condition of the house. If you’re unsure of how much you should budget, ask your realtor for some guidance.

HOA Fees (Homeowners Association Fees):

If your home is part of a community with an HOA, expect to pay fees for shared services and amenities. Research the rules and costs before purchasing.

Monthly Utility Bills:

You’ll need to pay for electricity, water, gas and internet. Over time, energy efficiency can lower costs. Initially budget for the full utility amounts.

Private Mortgage Insurance (Often referred to as PMI):

If your down payment is under 20% of the purchase price, you may be required to pay PMI to protect the lender if you default. Once you build equity, you may remove this expense.

Closing Costs:

Fees for loan origination, title insurance, attorneys and more add up at closing. Budget 2-5% of the home price for these upfront costs. Your Thompson Kane mortgage loan officer will always be transparent about closing costs and is a resource you can lean on throughout the home buying process to help you understand closing costs.

Consider all these expenses as you plan your budget. Understanding the true costs of homeownership helps you make smart financial decisions.

Related Posts